After more than 35 years of operation, TBI is closing its doors and our website will no longer be updated daily. Thank you for all of your support.

TBI Tech & Analysis: Picking apart Western Europe’s pay-TV & OTT markets

Rosie Molloy Gives Up Everything

Western Europe’s pay-TV and OTT operators secured more than 300 million subscribers in 2021, with streaming fuelling a year-on-year uptick of 26 million customers overall. However, that only tells part of the story, as Omdia’s Rob Moyser, Tony Gunnarsson, Matt Evenson & Max Signorelli explain.

Subscribers in Western Europe have been a key target for streaming operators for years, but that does not mean that the region’s pay-TV industry is set to disappear anytime soon.

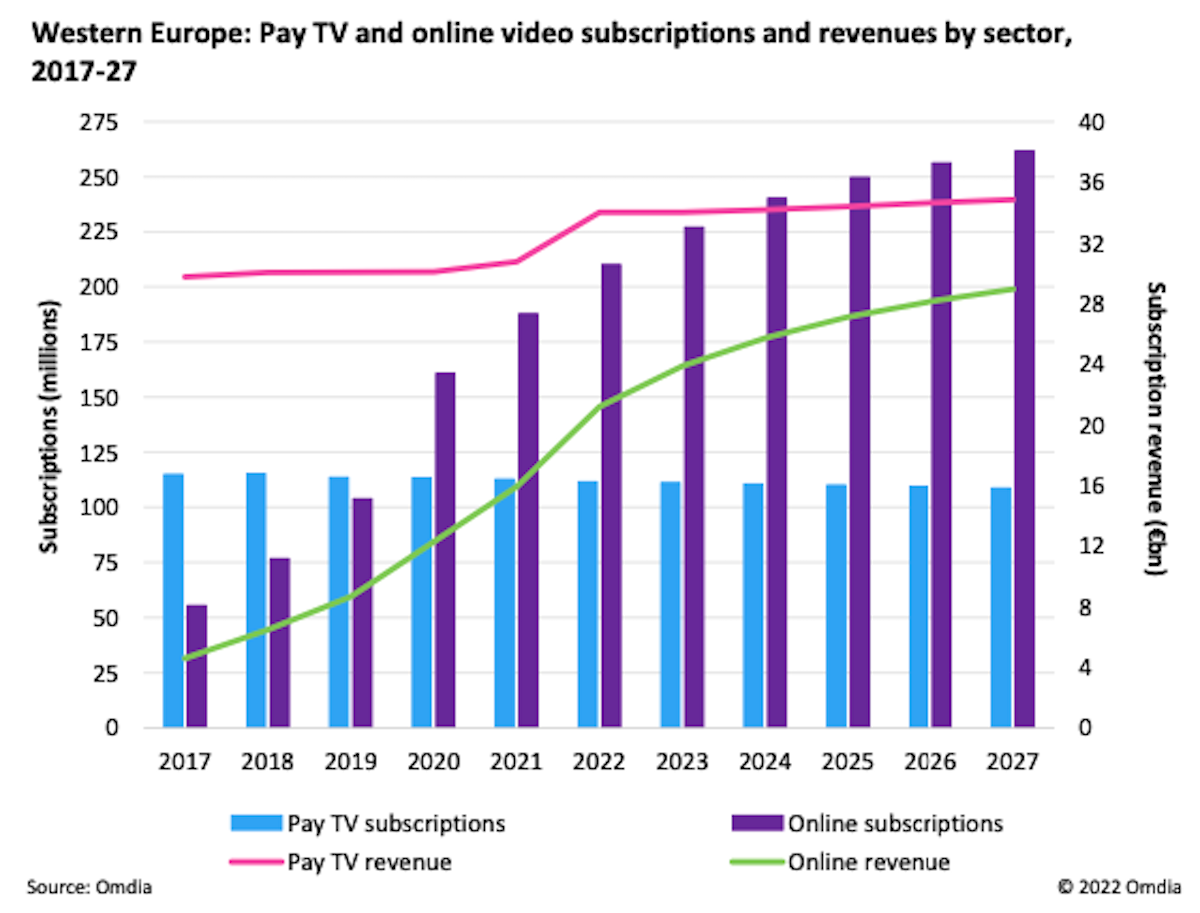

Total pay-TV and OTT subscriptions reached 300.5 million customers in 2021, adding 26.2 million customers over the year and nearly doubling in size since 2016, according to Omdia’s Pay TV & Online Video Report: Western Europe – 2022.

Sweden & Portugal have the highest pay-TV penetration in the region with a 97% share each

This growth came from the OTT market with subscriptions up by 26.9 million, while the pay-TV market contracted for a third consecutive year, losing 674,430 customers. However, this only equates to a 0.6% decline.

OTT subscriptions are now ahead of the pay-TV market by 74.9 million customers in 2021, reaching 187.7 million customers to pay-TV’s 112.7 million. Pay-TV revenue, however, continued to generate far greater profits with revenue almost double the size of the OTT market.

Netflix is the most popular OTT video service in Western Europe in 2021, with 62.4 million customers, accounting for a third of the total OTT market. Revenue has also risen accordingly, with profits rising to €7.3bn ($7.3bn) in 2021 moving to €9bn in 2022.

Pay-TV’s pitch versus OTT

For the pay-TV market in Western Europe, Vodafone is the clear leader with 15.4 million customers, with 84% of its customer base coming from its German pay-TV service.

As a combined unit, however, Sky generates the most revenue – €10.2bn. The company, which unveiled plans in May to launch more than 200 originals earlier this year with shows such as The Tattooist of Auschwitz and comedy Rosie Molloy Gives Up Everything, has an extensive presence in the region (the UK, Germany, Italy, Austria, and Ireland).

Several new D2C players launched in Western Europe in 2021. On January 5, 2021, Dplay was replaced by Discovery+ across 11 markets in Western Europe. It was then released in Germany and Austria in June 2022, but has yet to launch in several key markets, including France and Portugal.

HBO Max, meanwhile, was launched in several of its key markets in 2021, opening in Spain and the Nordic region in October 2021. This was later followed by Portugal and the Netherlands in March 2022. The merger between Discovery and WarnerMedia in March 2022, however, has complicated this matter even further with the two SVOD services set to merge as a combined OTT service in the summer of 2023.

Paramount+ was another D2C player that launched in Western Europe in 2021, becoming available in the Nordics in March 2021. This was followed by the UK and Ireland in July 2022, and is set to launch across the rest of Europe in 4Q22.

Local German OTT player RTL Now Premium also relaunched as RTL+ in June 2021, adding a whole host of media services, including music, books, magazines, and podcasts to its streaming service.

(Click to expand)

Stalwart nations

Pay-TV was particularly strong in France in 2021 with nearly a million customers added to reach a total of 25 million customers. Growth across all its main pay-TV operators, and platforms, account for this with operators such as Canal+, Free Telecom and Orange generating significant uptake.

Indeed, for companies such as Canal+, this is quite a turnaround as it had been in terminal decline (2013–19) for several years prior to 2020.

Germany remains the largest pay-TV base in the region with 27.9 million customers in 2021, accounting for a quarter of the region’s total. The country also leads in pay-TV revenue, generating €6.9bn ($6.9bn) in 2021.

Italy and Spain saw the most significant declines in their subscriber bases in 2021, with DAZN’s acquisition of the key soccer leagues from the countries top pay-TV operators Sky Italia (Seria A) and Telefónica (now partial rights holders to La Liga) playing a significant role in customer churn.

On top of this, continual growth from incumbents (Netflix, Disney+) and a wider variety of local content has driven many consumers to cord cut at a faster rate.

Sweden and Portugal have the highest pay-TV penetration in the region with a 97% share each, with Portugal seeing the largest increase in its pay-TV penetration over the past decade, moving from 72.4% to 97%.

Pay-TV penetration is below 60% in six markets, including three of the big five – a strong free-to-air offering in the UK, Italy, and Spain is one of the main factors holding back traditional pay-TV’s growth.

The edited excerpt above is from the Pay TV & Online Video Report: Western Europe – 2022 report, published by Omdia (a part of Informa, like TBI). It has been written by Rob Moyser, senior analyst for TV & Online; Tony Gunnarsson, principal analyst for TV & Online; Matt Evenson, research analyst for TV & Online; and Max Signorelli, senior analyst for TV & Online. For more info, click here.