After more than 35 years of operation, TBI is closing its doors and our website will no longer be updated daily. Thank you for all of your support.

TBI Tech & Analysis: Exploring global production trends into 2023

Lupin

Ahead of the Media & Entertainment Leaders Summit on Wednesday (see here), Richard Middleton hears from Omdia’s Tim Westcott about the key trends on the global production landscape to explore where opportunities lie in 2023 and beyond.

It has been a tumultuous few years for the global production industry, following the pandemic, health-related cost additions and subsequent talent shortages.

Factor that into an industry that saw broadcaster advertising revenues drop 10% worldwide in 2020, and the subsequent bounce-back for production has been swift.

It is important to note that much of the growth in revenues testifies to a recovery in commissioning, as well as a resurgence of mergers and acquisitions.

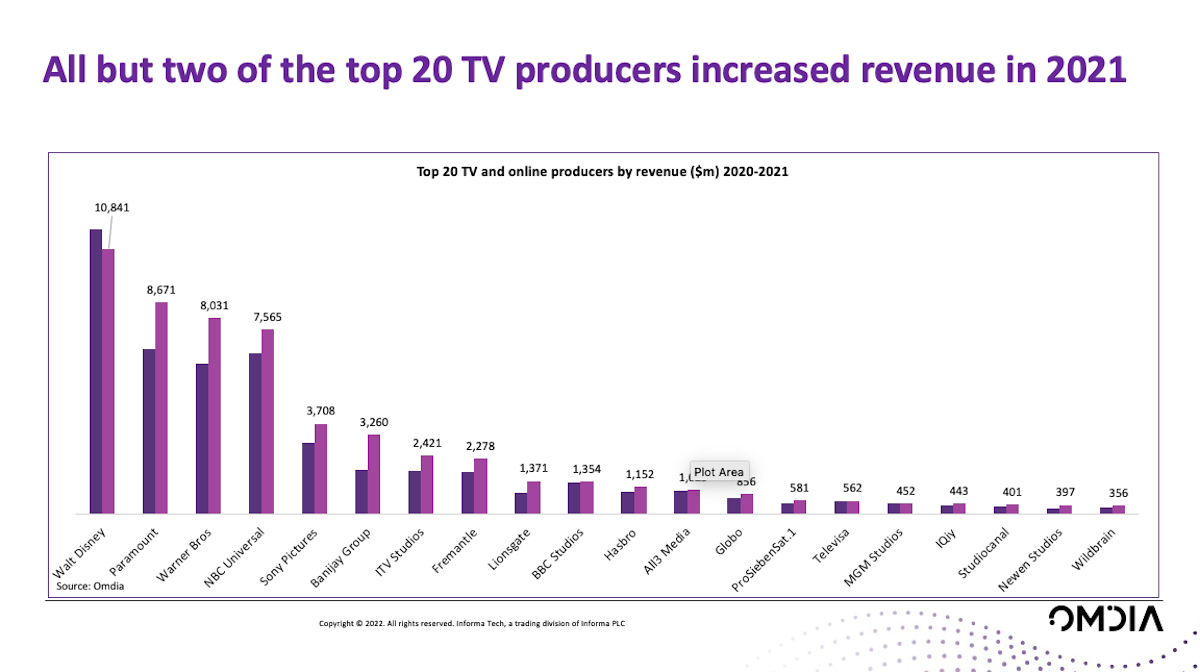

While 18 of the top 20 TV producers worldwide increased revenue in 2021 compared with 2020, it was France’s Gaumont that saw its television division report a 178% rise in sales, mainly due to Netflix commissions such as Lupin.

Another France-based comapny, Banijay, saw its revenue jump 79% in 2021, largely because of the consolidation of Endemol Shine Group, and there were also noticeable performances from companies such as South Korea’s JTBC.

Now rebranded Studio LuluLaLa, it rode the wave of Korean content success and has also been on its own M&A drive, snapping up Wiip, the independent production firm behind HBO series Mare Of Easttown.

Now rebranded Studio LuluLaLa, it rode the wave of Korean content success and has also been on its own M&A drive, snapping up Wiip, the independent production firm behind HBO series Mare Of Easttown.

The deal also neatly highlights how interconnected the global production industry is: it only arose after US-based Creative Artists Agency (CAA) agreed to sell its majority stake in the company as part of a pact to end the long standoff between agencies and the Writers Guild Of America.

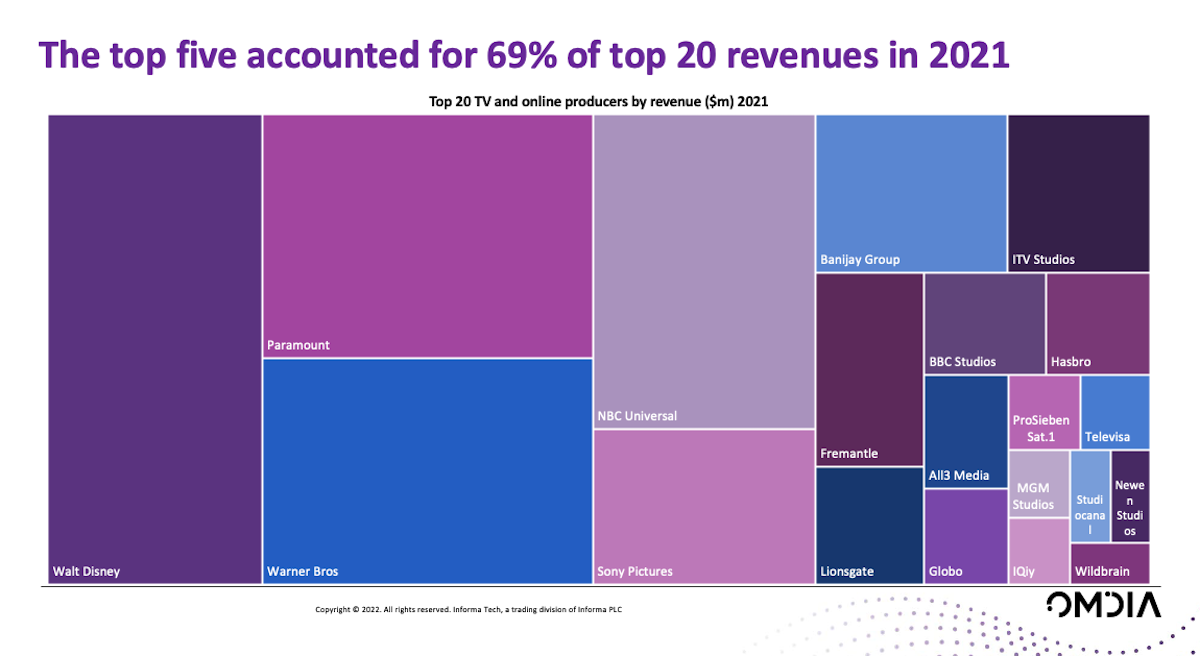

Nevertheless, the US continued to dominate the global production business last year, with Disney, Paramount, Warner Bros. Discovery, NBCUniversal and Sony Pictures accounting or almost 70% of the top 20 revenues.

Banijay topped companies outside of the US, with ITV Studios, Fremantle, All3Media and BBC Studios among the key European firms, while Globo remained a huge force in Latin America.

M&A has continued apace into 2022: Omdia has tracked 61 production company M&A deals (takeovers, investments, start-ups) already this year, with France replacing the UK as the most active buyer.

That has largely been driven by companies such as Banijay, Newen and Asacha building their networks, while other notable deals saw Amazon pay $8.5bn for MGM Studios. That was the biggest deal since Hasbro acquired Entertainment One in 2019 for $4.6bn.

That has largely been driven by companies such as Banijay, Newen and Asacha building their networks, while other notable deals saw Amazon pay $8.5bn for MGM Studios. That was the biggest deal since Hasbro acquired Entertainment One in 2019 for $4.6bn.

And while production revenues picked up in 2021, increasing investment from streamers was matched by traditional broadcasters, boding well for the future.

Indeed, the outlook is positive, with the studio-backed D2Cs stepping up original programming as they expand internationally, despite cost-cutting in certain regions.

However, the threat of economic slowdown and recession in some markets will impact investment by broadcasters reliant on advertising.

Producers are also contending with rising costs and competition for talent and studio space, with the omnipresent calls for streamers to offer more flexible terms on IP also becoming louder.

Tim Westcott is senior principal analyst for digital content & channels at Omdia which, like TBI, is part of Informa.

The excerpts above will be presented at the Media & Entertainment Leaders Summit during a panel featuring Banijay UK chairman Patrick Holland, Sky Studios COO Caroline Cooper and Red Planet Pictures’ joint-MD Alex Jones. To find out more & to book your place, click here.